America’s Steel Tariffs: Geopolitics, Industrial Muscle, and the Next Supply Chain Domino

May 31, 2025

Trump’s plan to double steel tariffs to 50% reignites the industrial policy debate, with ripple effects for global supply chains, manufacturing costs, and the new age of “resource nationalism.” Here’s what’s at stake—and where the real market shocks could land.

U.S. Steel Tariffs: Back to the Future of Industrial Policy

If you want a live case study in “resource nationalism,” look no further than the White House’s latest steel move: Trump has announced plans to double U.S. tariffs on steel imports from 25% to 50%, with the stated goal of locking in domestic jobs, protecting U.S. Steel, and shoring up American manufacturing muscle.

But this is bigger than campaign theater. The U.S. is sending a clear message: industrial sovereignty and political leverage now trump decades of global free-market orthodoxy.

What’s Actually Happening: 50% Tariff, New Steel Deal

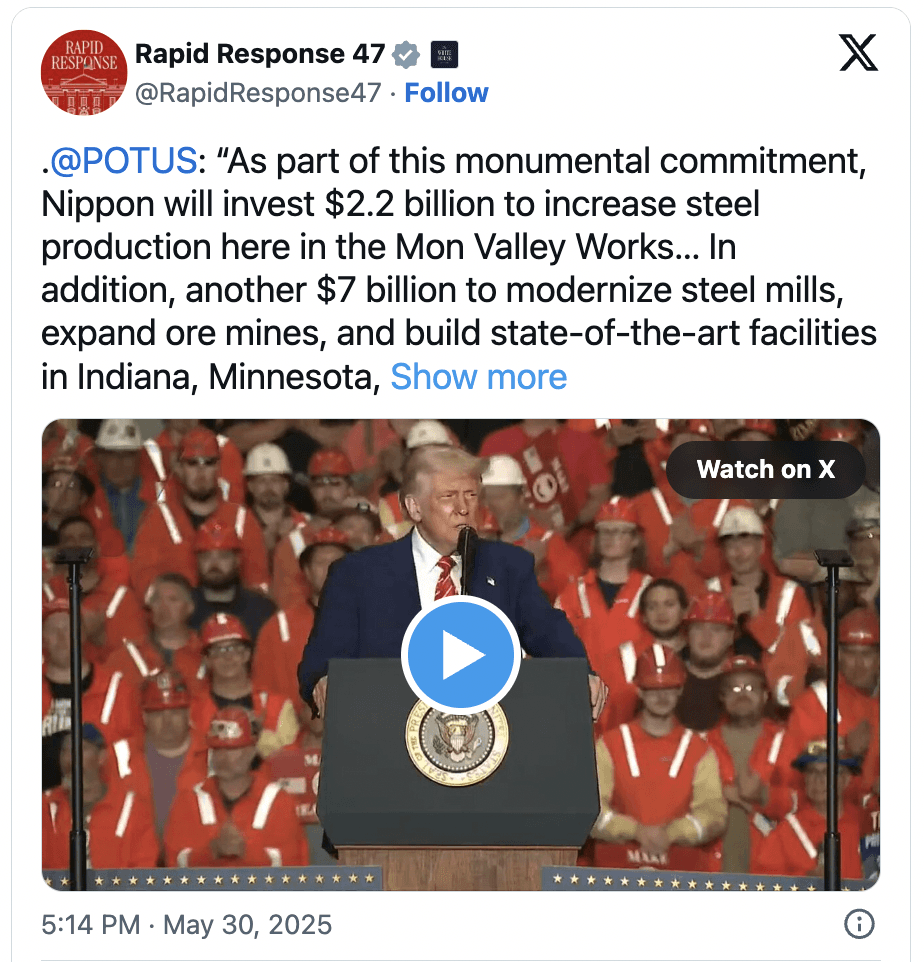

The details: The proposed tariff hike comes alongside an expected U.S. Steel–Nippon Steel partnership, with the deal structured to keep U.S. Steel “American-owned and operated,” at least in legal form.

Trump: “We’re going to bring it from 25% to 50% on steel into the United States of America, which will even further secure the steel industry in the United States.” [source]

Nippon Steel has pledged over $14 billion in U.S. investments, promising at least 70,000 jobs and major upgrades to steelmaking infrastructure.

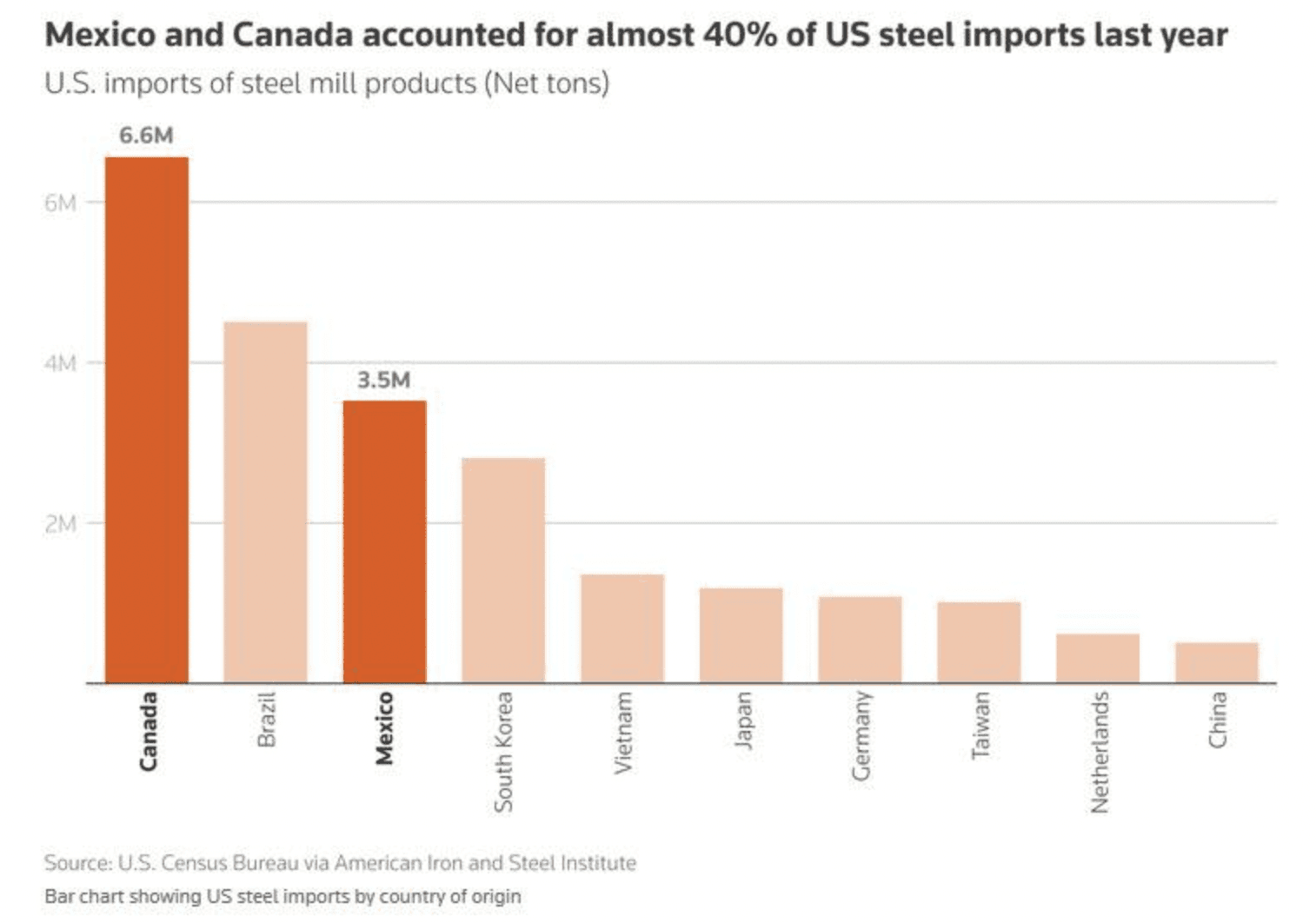

The Data: Where U.S. Steel Imports Come From

The five biggest sources of steel imports to the U.S.:

Canada (largest by far)

Brazil

Mexico

South Korea

Vietnam

Canada and Mexico account for nearly 40% of U.S. steel imports—meaning the new tariffs hit close to home in North America’s integrated supply chain. [source]

Market Impact: Who Wins, Who Loses?

U.S. steel producers: Stocks like Nucor, Cleveland-Cliffs, and Steel Dynamics rallied immediately after the news. Expect more volatility as investors bet on policy uncertainty.

Manufacturers: Auto, construction, and appliance makers are bracing for higher input costs—steel is embedded in every layer of the real economy.

Trading partners: Canada, Mexico, Brazil, and South Korea are likely to pursue exemptions or retaliatory measures, escalating trade tensions.

The Industrial Strategy Angle: More Than Just Jobs

Tariffs aren’t just about protecting steel jobs. They’re a signal to global competitors and allies that supply chain resilience and domestic control now trump cheap imports. The U.S. is following a playbook now familiar from Europe, India, and China: limit exposure, boost self-reliance, and weaponize the supply chain as a strategic tool.

Global context: Since 2018, over 30 countries have implemented some form of steel protectionism or quota. [source]

Capacity utilization: U.S. steel mills still run below the 85% “healthy” threshold, while Chinese overcapacity keeps global prices structurally depressed. [link here]

Geopolitics, Trade Wars, and the “American Steel” Brand

Japan-U.S. deal: The Nippon Steel/US Steel partnership is the new battleground in the U.S.-Japan economic relationship—expect CFIUS review, union resistance, and ongoing political drama.

National security: Both Biden and Trump have cited security risk to justify keeping US Steel “in American hands.”

Historical echoes: The rhetoric—“Decades of Washington betrayal and incompetence…they melted away just like butter melts away”—echoes 1980s and 2000s deindustrialization narratives, but with new urgency in an era of great power competition.

Why This Story Matters

Steel is the backbone of industrial civilization. How America handles its supply, pricing, and strategic partnerships will set the tone for the next decade of manufacturing and geopolitics. For commodity players, manufacturers, and policy watchers, this is the real story: Tariffs are no longer a sideshow—they’re core to the new global rules of engagement.

The Gamp Sheet will be watching the next moves: trade retaliation, CFIUS reviews, and how supply chain players adapt in the age of managed trade.

The Lean Revolution: Why America’s Biggest Companies Are Slashing White-Collar Jobs—and What It Means for the Global Economy ›

America’s Steel Tariffs: Geopolitics, Industrial Muscle, and the Next Supply Chain Domino

May 31, 2025

Trump’s plan to double steel tariffs to 50% reignites the industrial policy debate, with ripple effects for global supply chains, manufacturing costs, and the new age of “resource nationalism.” Here’s what’s at stake—and where the real market shocks could land.

U.S. Steel Tariffs: Back to the Future of Industrial Policy

If you want a live case study in “resource nationalism,” look no further than the White House’s latest steel move: Trump has announced plans to double U.S. tariffs on steel imports from 25% to 50%, with the stated goal of locking in domestic jobs, protecting U.S. Steel, and shoring up American manufacturing muscle.

But this is bigger than campaign theater. The U.S. is sending a clear message: industrial sovereignty and political leverage now trump decades of global free-market orthodoxy.

What’s Actually Happening: 50% Tariff, New Steel Deal

The details: The proposed tariff hike comes alongside an expected U.S. Steel–Nippon Steel partnership, with the deal structured to keep U.S. Steel “American-owned and operated,” at least in legal form.

Trump: “We’re going to bring it from 25% to 50% on steel into the United States of America, which will even further secure the steel industry in the United States.” [source]

Nippon Steel has pledged over $14 billion in U.S. investments, promising at least 70,000 jobs and major upgrades to steelmaking infrastructure.

The Data: Where U.S. Steel Imports Come From

The five biggest sources of steel imports to the U.S.:

Canada (largest by far)

Brazil

Mexico

South Korea

Vietnam

Canada and Mexico account for nearly 40% of U.S. steel imports—meaning the new tariffs hit close to home in North America’s integrated supply chain. [source]

Market Impact: Who Wins, Who Loses?

U.S. steel producers: Stocks like Nucor, Cleveland-Cliffs, and Steel Dynamics rallied immediately after the news. Expect more volatility as investors bet on policy uncertainty.

Manufacturers: Auto, construction, and appliance makers are bracing for higher input costs—steel is embedded in every layer of the real economy.

Trading partners: Canada, Mexico, Brazil, and South Korea are likely to pursue exemptions or retaliatory measures, escalating trade tensions.

The Industrial Strategy Angle: More Than Just Jobs

Tariffs aren’t just about protecting steel jobs. They’re a signal to global competitors and allies that supply chain resilience and domestic control now trump cheap imports. The U.S. is following a playbook now familiar from Europe, India, and China: limit exposure, boost self-reliance, and weaponize the supply chain as a strategic tool.

Global context: Since 2018, over 30 countries have implemented some form of steel protectionism or quota. [source]

Capacity utilization: U.S. steel mills still run below the 85% “healthy” threshold, while Chinese overcapacity keeps global prices structurally depressed. [link here]

Geopolitics, Trade Wars, and the “American Steel” Brand

Japan-U.S. deal: The Nippon Steel/US Steel partnership is the new battleground in the U.S.-Japan economic relationship—expect CFIUS review, union resistance, and ongoing political drama.

National security: Both Biden and Trump have cited security risk to justify keeping US Steel “in American hands.”

Historical echoes: The rhetoric—“Decades of Washington betrayal and incompetence…they melted away just like butter melts away”—echoes 1980s and 2000s deindustrialization narratives, but with new urgency in an era of great power competition.

Why This Story Matters

Steel is the backbone of industrial civilization. How America handles its supply, pricing, and strategic partnerships will set the tone for the next decade of manufacturing and geopolitics. For commodity players, manufacturers, and policy watchers, this is the real story: Tariffs are no longer a sideshow—they’re core to the new global rules of engagement.

The Gamp Sheet will be watching the next moves: trade retaliation, CFIUS reviews, and how supply chain players adapt in the age of managed trade.

The Lean Revolution: Why America’s Biggest Companies Are Slashing White-Collar Jobs—and What It Means for the Global Economy ›