Iron Ore’s Warning: China’s Slowdown Is Sending Shockwaves Through Global Metals

Jun 19, 2025

Iron ore prices just hit a 9-month low, with Citi and Goldman slashing targets. What’s behind the drop? China’s steel and property market malaise is a red flag for global demand and a test for anyone betting on a quick industrial rebound.

Iron Ore Slumps—And the Global Economy Needs to Pay Attention

If you want to know where global industry is headed, watch iron ore—and right now, it’s flashing red.

Prices have tumbled below $93 a ton, the lowest since Q3 2024, as sluggish Chinese demand collides with record exports and a steel sector stuck in low gear (ZeroHedge).

Why does this matter? Iron ore is the world’s industrial barometer, setting the pace for steel, infrastructure, and the broader global cycle. When China—the buyer of more than 70% of seaborne iron ore—catches a cold, the world’s commodity producers feel the chill.

Steel, Property, and Deflation: The Triple Threat in China

The current drop isn’t just about prices.

Steel output in China fell 7% year-on-year in May, the weakest since 2018 (ZeroHedge).

Property sector malaise: China’s real estate sector is still seeing negative growth and record developer defaults (Bloomberg). Steel demand from construction is likely to remain soft for months.

Deflationary drag: Consumer prices in China have hovered at or below zero for much of 2024, a sign that stimulus isn’t translating into real growth (Trading Economics).

Goldman Sachs and Citi have both cut their iron ore forecasts to $85–$90/ton for the next year, down from $100+ earlier in 2024. Analyst James McGeoch:

“There is a flat price call that you can play the $90–95 range, however it’s a downward sloping trend.”

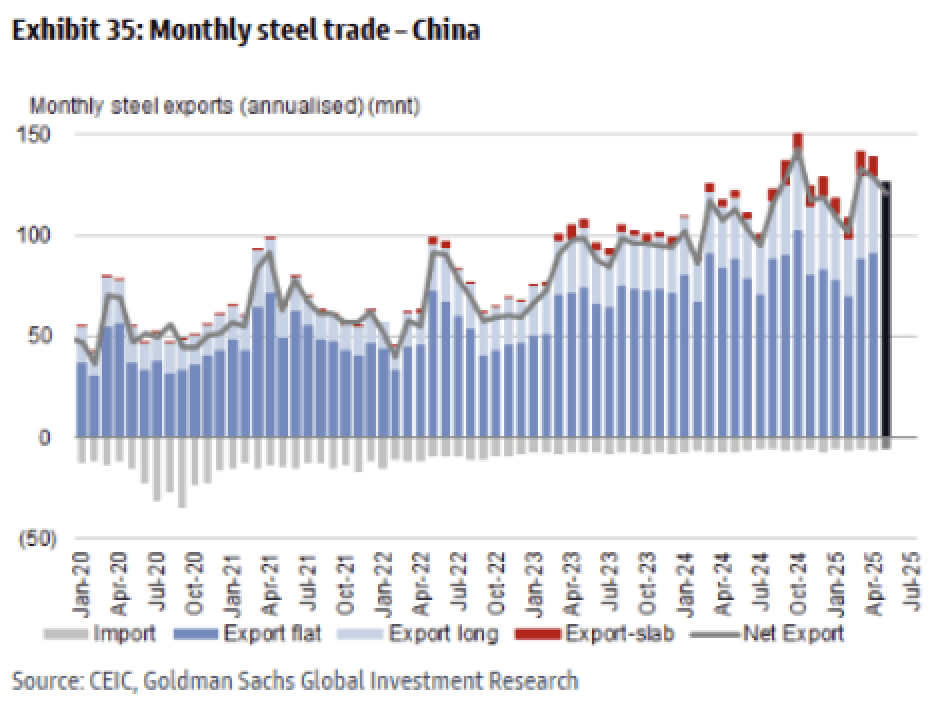

The Export Paradox: Chinese Steel Floods Global Markets

Despite weak domestic demand, China’s steel exports are booming:

Export volumes remain elevated, with monthly shipments at multi-year highs (Goldman chart; see also ZeroHedge article charts).

This is softening the blow for Chinese mills—but undercuts prices and squeezes margins for global competitors, from India to Europe and the Americas (World Steel Association).

The upshot: China’s pain is exporting deflation and margin pressure across the world’s steel and industrial sectors.

Why This Matters: Commodity Supercycle or Synchronized Stall?

The iron ore plunge isn’t just a China story.

Global miners (like Vale, Rio Tinto, BHP) depend on Chinese demand for profit. Their margins are now under threat, with investment plans and jobs in Australia, Brazil, and Africa at risk (BHP results).

Shipping & trade: Lower iron ore and steel volumes mean weaker demand for bulk shipping, rippling into freight rates (Baltic Dry Index).

Macro signal: If China can’t reignite its construction and manufacturing engine, global hopes for a late-2025 industrial bounce may be misplaced.

The Gamp Sheet Take: Don’t Trust the Bottom Yet

Commodity traders betting on a quick iron ore rebound should stay cautious.

All major signals—steel output, property, price targets—are pointing sideways or down.

Until China’s property and credit cycle genuinely turn, the floor for iron ore (and the global supercycle narrative) remains shaky.

Final thought:

Watch for any policy bazooka from Beijing or a surprise restock from Indian and ASEAN buyers. But for now, iron ore is telling the truth—and it’s not bullish.

Sources

The Lean Revolution: Why America’s Biggest Companies Are Slashing White-Collar Jobs—and What It Means for the Global Economy ›

Iron Ore’s Warning: China’s Slowdown Is Sending Shockwaves Through Global Metals

Jun 19, 2025

Iron ore prices just hit a 9-month low, with Citi and Goldman slashing targets. What’s behind the drop? China’s steel and property market malaise is a red flag for global demand and a test for anyone betting on a quick industrial rebound.

Iron Ore Slumps—And the Global Economy Needs to Pay Attention

If you want to know where global industry is headed, watch iron ore—and right now, it’s flashing red.

Prices have tumbled below $93 a ton, the lowest since Q3 2024, as sluggish Chinese demand collides with record exports and a steel sector stuck in low gear (ZeroHedge).

Why does this matter? Iron ore is the world’s industrial barometer, setting the pace for steel, infrastructure, and the broader global cycle. When China—the buyer of more than 70% of seaborne iron ore—catches a cold, the world’s commodity producers feel the chill.

Steel, Property, and Deflation: The Triple Threat in China

The current drop isn’t just about prices.

Steel output in China fell 7% year-on-year in May, the weakest since 2018 (ZeroHedge).

Property sector malaise: China’s real estate sector is still seeing negative growth and record developer defaults (Bloomberg). Steel demand from construction is likely to remain soft for months.

Deflationary drag: Consumer prices in China have hovered at or below zero for much of 2024, a sign that stimulus isn’t translating into real growth (Trading Economics).

Goldman Sachs and Citi have both cut their iron ore forecasts to $85–$90/ton for the next year, down from $100+ earlier in 2024. Analyst James McGeoch:

“There is a flat price call that you can play the $90–95 range, however it’s a downward sloping trend.”

The Export Paradox: Chinese Steel Floods Global Markets

Despite weak domestic demand, China’s steel exports are booming:

Export volumes remain elevated, with monthly shipments at multi-year highs (Goldman chart; see also ZeroHedge article charts).

This is softening the blow for Chinese mills—but undercuts prices and squeezes margins for global competitors, from India to Europe and the Americas (World Steel Association).

The upshot: China’s pain is exporting deflation and margin pressure across the world’s steel and industrial sectors.

Why This Matters: Commodity Supercycle or Synchronized Stall?

The iron ore plunge isn’t just a China story.

Global miners (like Vale, Rio Tinto, BHP) depend on Chinese demand for profit. Their margins are now under threat, with investment plans and jobs in Australia, Brazil, and Africa at risk (BHP results).

Shipping & trade: Lower iron ore and steel volumes mean weaker demand for bulk shipping, rippling into freight rates (Baltic Dry Index).

Macro signal: If China can’t reignite its construction and manufacturing engine, global hopes for a late-2025 industrial bounce may be misplaced.

The Gamp Sheet Take: Don’t Trust the Bottom Yet

Commodity traders betting on a quick iron ore rebound should stay cautious.

All major signals—steel output, property, price targets—are pointing sideways or down.

Until China’s property and credit cycle genuinely turn, the floor for iron ore (and the global supercycle narrative) remains shaky.

Final thought:

Watch for any policy bazooka from Beijing or a surprise restock from Indian and ASEAN buyers. But for now, iron ore is telling the truth—and it’s not bullish.

Sources

The Lean Revolution: Why America’s Biggest Companies Are Slashing White-Collar Jobs—and What It Means for the Global Economy ›