When 52% Ownership Isn’t Enough: Japan’s Bond Market Breaks

May 26, 2025

Japan's bond market is quietly blowing up — and the central bank that owns over half of it is nowhere to be found.

Japan's bond market is quietly blowing up — and the central bank that owns over half of it is nowhere to be found.

Last week, Japanese life insurers dumped long-duration government bonds (JGBs) at the fastest pace on record. Meiji Yasuda, Sumitomo, Dai-ichi, and Nippon Life — four of Japan’s largest — reported a combined ¥8.5 trillion ($54 billion) in unrealized bond losses for the fiscal year, a 4x increase from a year prior.

📉 BOJ owns 52% of all JGBs. And yet, yields on 30- and 40-year JGBs spiked to levels not seen since the 1980s — a direct breakdown in the very market the Bank of Japan is supposed to control.

Why this is bigger than it looks:

40Y JGB yields surged after a dismal 20Y auction — the worst bid-to-cover since 2012.

The "tail" on that auction (i.e., difference between the high yield and average accepted) was the largest since 1987 — a sign of zero real demand.

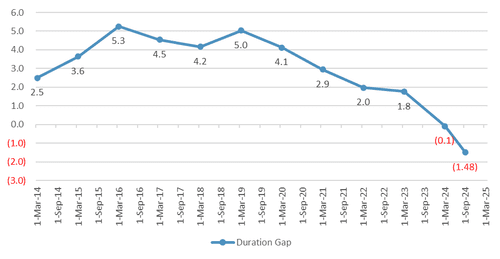

Japanese lifers now hold such massive duration gaps that their solvency math breaks at any spike in rates. The latest estimates show the duration gap at -1.48 years, a sharp plunge from positive territory just 2 years ago.

Monthly net purchases of long-end JGBs by life insurers turned deeply negative, implying they’re not just slowing purchases — they’re actively dumping bonds.

This isn’t a liquidity rotation. It’s an institutional exodus.

The Domino Setup: Contagion Risk in Asia

If you think this is just a domestic Japan issue, you’re missing the bigger picture.

Japanese insurers are some of the largest allocators in global fixed income, often parking cash in U.S. Treasuries, European sovereigns, and Asian corporate bonds. When their domestic portfolio melts down, they don’t just stop buying abroad — they sell.

This adds a layer of fragility across:

🇺🇸 U.S. Treasuries – Japan is still the #1 foreign holder.

🇪🇺 European bonds – Already fragile post-Ukraine.

🌏 Asian credit – Where liquidity is shallow and correlated to Japan’s financial health.

Remember: the Bank of Japan already tried to play this game by yield-curve-controlling the entire long end. But that only muted the signals — it didn’t remove the risk. Now that those same yields are screaming higher outside the BOJ’s direct control (30Y, 40Y), the pressure is blowing out through the insurance sector.

The BOJ is pretending nothing is happening.

That’s the headline from ZeroHedge, and it’s hard to argue. When the world’s second-largest bond market becomes bidless and the central bank is both the buyer of last resort and the primary bagholder, we’re watching a monetary experiment end in real time.

The question isn't whether Japan can contain this — it's whether other markets are prepared for what happens if they can’t.

The Lean Revolution: Why America’s Biggest Companies Are Slashing White-Collar Jobs—and What It Means for the Global Economy ›

When 52% Ownership Isn’t Enough: Japan’s Bond Market Breaks

May 26, 2025

Japan's bond market is quietly blowing up — and the central bank that owns over half of it is nowhere to be found.

Japan's bond market is quietly blowing up — and the central bank that owns over half of it is nowhere to be found.

Last week, Japanese life insurers dumped long-duration government bonds (JGBs) at the fastest pace on record. Meiji Yasuda, Sumitomo, Dai-ichi, and Nippon Life — four of Japan’s largest — reported a combined ¥8.5 trillion ($54 billion) in unrealized bond losses for the fiscal year, a 4x increase from a year prior.

📉 BOJ owns 52% of all JGBs. And yet, yields on 30- and 40-year JGBs spiked to levels not seen since the 1980s — a direct breakdown in the very market the Bank of Japan is supposed to control.

Why this is bigger than it looks:

40Y JGB yields surged after a dismal 20Y auction — the worst bid-to-cover since 2012.

The "tail" on that auction (i.e., difference between the high yield and average accepted) was the largest since 1987 — a sign of zero real demand.

Japanese lifers now hold such massive duration gaps that their solvency math breaks at any spike in rates. The latest estimates show the duration gap at -1.48 years, a sharp plunge from positive territory just 2 years ago.

Monthly net purchases of long-end JGBs by life insurers turned deeply negative, implying they’re not just slowing purchases — they’re actively dumping bonds.

This isn’t a liquidity rotation. It’s an institutional exodus.

The Domino Setup: Contagion Risk in Asia

If you think this is just a domestic Japan issue, you’re missing the bigger picture.

Japanese insurers are some of the largest allocators in global fixed income, often parking cash in U.S. Treasuries, European sovereigns, and Asian corporate bonds. When their domestic portfolio melts down, they don’t just stop buying abroad — they sell.

This adds a layer of fragility across:

🇺🇸 U.S. Treasuries – Japan is still the #1 foreign holder.

🇪🇺 European bonds – Already fragile post-Ukraine.

🌏 Asian credit – Where liquidity is shallow and correlated to Japan’s financial health.

Remember: the Bank of Japan already tried to play this game by yield-curve-controlling the entire long end. But that only muted the signals — it didn’t remove the risk. Now that those same yields are screaming higher outside the BOJ’s direct control (30Y, 40Y), the pressure is blowing out through the insurance sector.

The BOJ is pretending nothing is happening.

That’s the headline from ZeroHedge, and it’s hard to argue. When the world’s second-largest bond market becomes bidless and the central bank is both the buyer of last resort and the primary bagholder, we’re watching a monetary experiment end in real time.

The question isn't whether Japan can contain this — it's whether other markets are prepared for what happens if they can’t.

The Lean Revolution: Why America’s Biggest Companies Are Slashing White-Collar Jobs—and What It Means for the Global Economy ›