A Hard Reset: Diamond Market Finds Its Floor, but Looming Supply Crunch Sets Up a Wild 2025–2029

Jun 19, 2025

After years in the dumps, the diamond market has (finally) bottomed, says UBS—but looming supply deficits, lab-grown disruption, and shifting consumer tastes mean the story is just getting interesting. Here’s what every trader, luxury analyst, and industrial strategist needs to know.

Bottom Found? Don’t Get Too Comfortable

The worst may be over for diamond prices, but for the industry, the real drama is just beginning.

After a brutal multi-year bear market driven by oversupply, macro headwinds, and the lab-grown revolution, UBS has called a “bottom”—but warns that a tightening supply through 2029 could send shocks through luxury and industrial supply chains (ZeroHedge).

The Data: Prices Stabilize as Supply Sinks

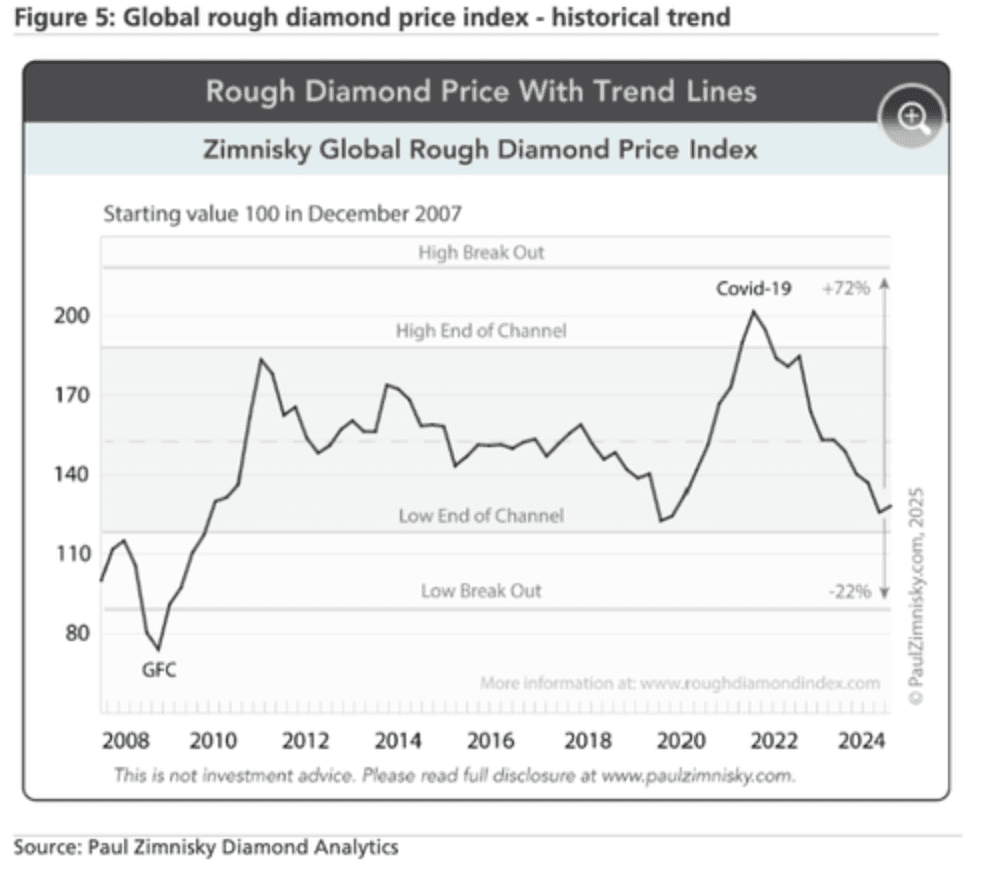

Natural diamond prices are modestly rebounding off multi-decade lows as De Beers and Alrosa slash supply.

High-quality stones are already up ~10% year-to-date, while most other categories are off the floor.

Market fundamentals look more supportive for the medium term, assuming demand picks up with ad spend and macro stabilization.

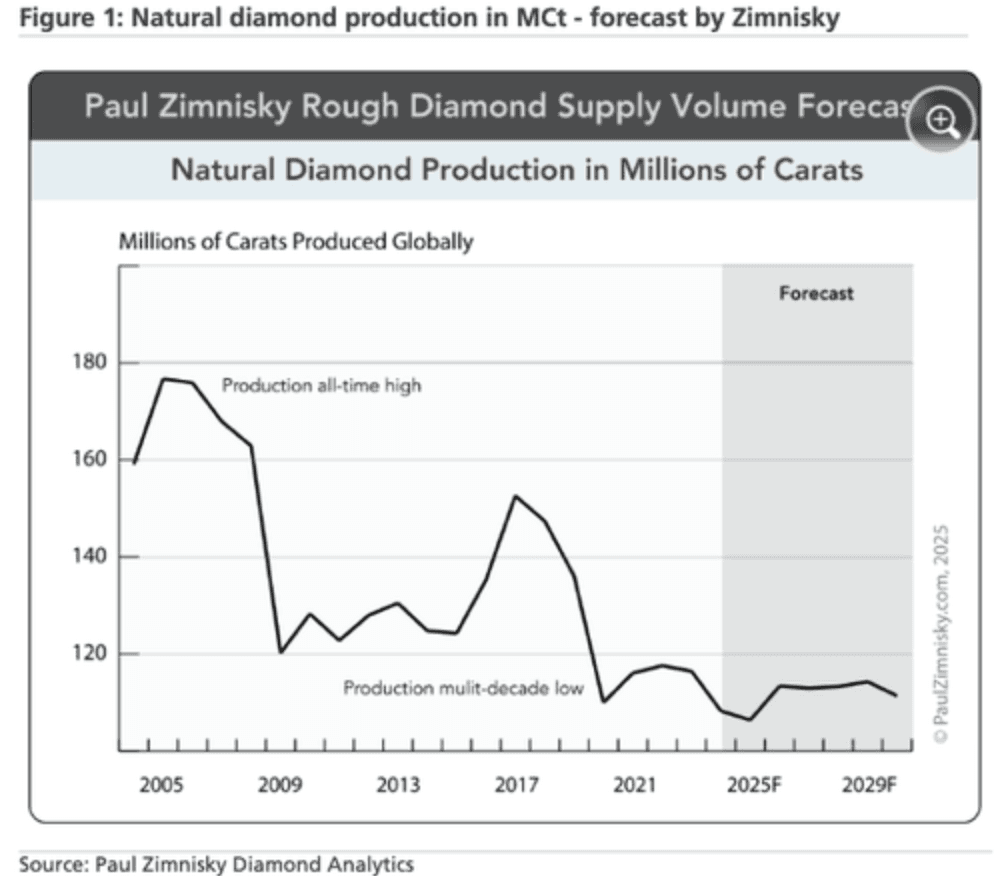

The chart below shows just how dramatic the drop in production has been—and how tight things could get as global output remains stuck at ~100–125 million carats/year, the lowest since the early 1990s (Zimnisky).

Why Supply Will Stay Tight: Mining, Lab-Grown, and Geopolitics

Most new natural diamond deposits are depleted; Africa’s Luaxe mine is the only major new project of scale, and it won’t move the needle for years.

Existing mega-mines (Jwaneng, Orapa, Venetia) still have decades of life but can’t offset lack of fresh supply (Paul Zimnisky interview).

Geopolitics: Russian diamonds (Alrosa) face sanctions risk; any further disruption could tighten the market quickly (Reuters).

UBS and Zimnisky both project natural production will fall as much as 50% from recent peaks by 2029, unless prices rise enough to restart exploration.

The Lab-Grown Factor: Disruption or Lifeline?

Lab-grown diamonds (LGDs) are the biggest wild card:

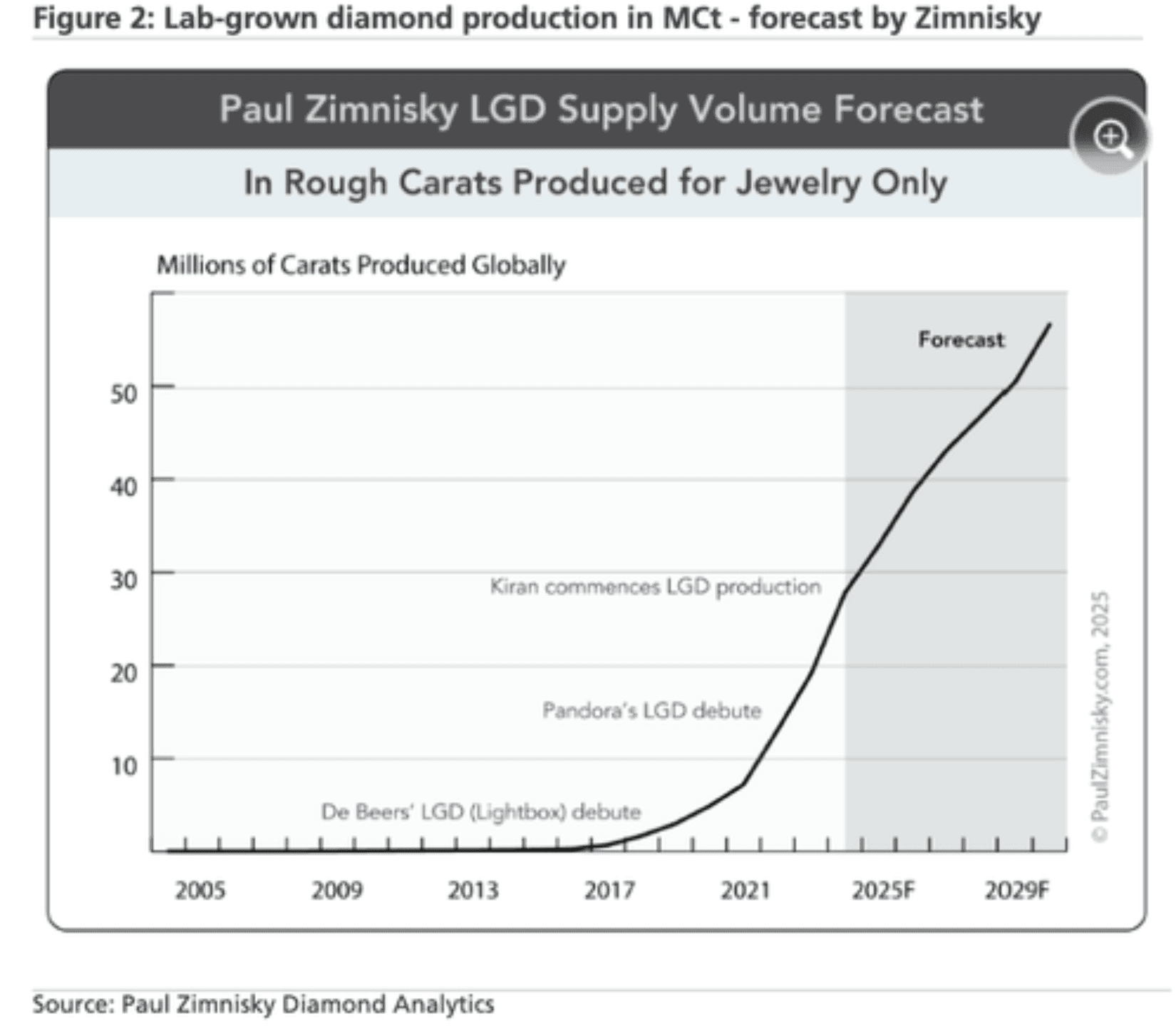

Production is exploding—Zimnisky forecasts LGD supply for jewelry will double from ~20 million carats in 2023 to ~50 million by 2028 (Zimnisky supply chart).

Prices for LGDs keep falling, with the polished index down 70% since 2016. This keeps real stones “rare”—but also dilutes mass-market jewelry value.

High-end consumers still vastly prefer natural, but LGDs are taking real share in entry and mid-level jewelry.

Market Outlook: Who Wins (and Who Should Worry)

De Beers (Anglo American) and Alrosa will control a bigger share of a shrinking market, making them both more valuable and more exposed to demand swings.

The next few years could see major consolidation, with luxury conglomerates, sovereign funds, or even tech buyers (think Apple, Tesla for industrial diamond applications) stepping in (Bloomberg).

For traders and hedge funds: expect volatility. Supply is set, but demand will swing on advertising, consumer sentiment, and geopolitics.

The Gamp Sheet Take: Diamonds Repricing Reality

This is not just a luxury story—it’s a microcosm of the next decade in commodities: chronic underinvestment, synthetic disruption, and high-stakes geopolitics.

If you’re a bull: The setup for a multi-year price squeeze is real, especially if inflation returns or China/India demand surprises to the upside.

If you’re a skeptic: Watch for LGDs to put a lid on prices and push more volume to mass-market jewelry and industrials.

For everyone else: The diamond market may have bottomed, but the next up-cycle will look nothing like the last.

Final thought:

If you want a case study in how global supply chains, branding, and macro policy collide—keep watching diamonds.

Sources

The Lean Revolution: Why America’s Biggest Companies Are Slashing White-Collar Jobs—and What It Means for the Global Economy ›

A Hard Reset: Diamond Market Finds Its Floor, but Looming Supply Crunch Sets Up a Wild 2025–2029

Jun 19, 2025

After years in the dumps, the diamond market has (finally) bottomed, says UBS—but looming supply deficits, lab-grown disruption, and shifting consumer tastes mean the story is just getting interesting. Here’s what every trader, luxury analyst, and industrial strategist needs to know.

Bottom Found? Don’t Get Too Comfortable

The worst may be over for diamond prices, but for the industry, the real drama is just beginning.

After a brutal multi-year bear market driven by oversupply, macro headwinds, and the lab-grown revolution, UBS has called a “bottom”—but warns that a tightening supply through 2029 could send shocks through luxury and industrial supply chains (ZeroHedge).

The Data: Prices Stabilize as Supply Sinks

Natural diamond prices are modestly rebounding off multi-decade lows as De Beers and Alrosa slash supply.

High-quality stones are already up ~10% year-to-date, while most other categories are off the floor.

Market fundamentals look more supportive for the medium term, assuming demand picks up with ad spend and macro stabilization.

The chart below shows just how dramatic the drop in production has been—and how tight things could get as global output remains stuck at ~100–125 million carats/year, the lowest since the early 1990s (Zimnisky).

Why Supply Will Stay Tight: Mining, Lab-Grown, and Geopolitics

Most new natural diamond deposits are depleted; Africa’s Luaxe mine is the only major new project of scale, and it won’t move the needle for years.

Existing mega-mines (Jwaneng, Orapa, Venetia) still have decades of life but can’t offset lack of fresh supply (Paul Zimnisky interview).

Geopolitics: Russian diamonds (Alrosa) face sanctions risk; any further disruption could tighten the market quickly (Reuters).

UBS and Zimnisky both project natural production will fall as much as 50% from recent peaks by 2029, unless prices rise enough to restart exploration.

The Lab-Grown Factor: Disruption or Lifeline?

Lab-grown diamonds (LGDs) are the biggest wild card:

Production is exploding—Zimnisky forecasts LGD supply for jewelry will double from ~20 million carats in 2023 to ~50 million by 2028 (Zimnisky supply chart).

Prices for LGDs keep falling, with the polished index down 70% since 2016. This keeps real stones “rare”—but also dilutes mass-market jewelry value.

High-end consumers still vastly prefer natural, but LGDs are taking real share in entry and mid-level jewelry.

Market Outlook: Who Wins (and Who Should Worry)

De Beers (Anglo American) and Alrosa will control a bigger share of a shrinking market, making them both more valuable and more exposed to demand swings.

The next few years could see major consolidation, with luxury conglomerates, sovereign funds, or even tech buyers (think Apple, Tesla for industrial diamond applications) stepping in (Bloomberg).

For traders and hedge funds: expect volatility. Supply is set, but demand will swing on advertising, consumer sentiment, and geopolitics.

The Gamp Sheet Take: Diamonds Repricing Reality

This is not just a luxury story—it’s a microcosm of the next decade in commodities: chronic underinvestment, synthetic disruption, and high-stakes geopolitics.

If you’re a bull: The setup for a multi-year price squeeze is real, especially if inflation returns or China/India demand surprises to the upside.

If you’re a skeptic: Watch for LGDs to put a lid on prices and push more volume to mass-market jewelry and industrials.

For everyone else: The diamond market may have bottomed, but the next up-cycle will look nothing like the last.

Final thought:

If you want a case study in how global supply chains, branding, and macro policy collide—keep watching diamonds.

Sources

The Lean Revolution: Why America’s Biggest Companies Are Slashing White-Collar Jobs—and What It Means for the Global Economy ›